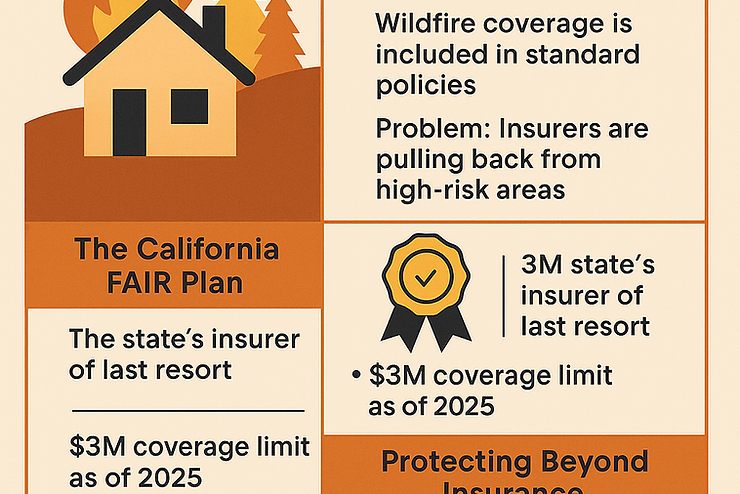

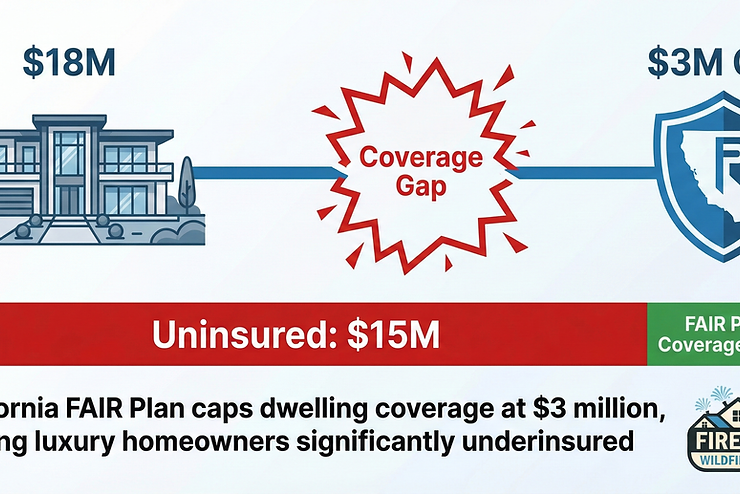

California FAIR Plan $3M Cap: Why Luxury Homes Need Wildfire Defense Systems

Shawn Gardner, Co-Founder

The solution that saved homes in the 2007 Ham Lake Fire still isn't standard in California's WUI.

This article explores the latest developments in wildfire defense, risk mitigation, and protection strategies for Bay Area homeowners. Understanding your property's unique exposure to wildfire, whether from terrain, vegetation, wind patterns, or proximity to wildland, is the first step toward meaningful protection.

For homes in Very High Fire Hazard Severity Zones across Saratoga, Los Gatos, Woodside, Los Altos Hills, and the Santa Cruz Mountains, the combination of automated detection and sprinkler defense represents the most effective approach currently available. The full article covers specific data, analysis, and actionable takeaways that homeowners in the WUI should understand.

Written by Shawn Gardner, Co-Founder of FireRoofs

Researched and reviewed by industry professionals.

Ready to Protect Your Home?

Every property out here is different. We'll walk yours for free and tell you exactly what it needs.

Book Free Home Evaluation