Standard homeowners insurance policies in the United States typically include fire coverage, which extends to wildfires. However, having coverage and being fully protected are two different things. The gap between these can have devastating financial consequences.

Many California homeowners have discovered this distinction too late. They maintained their policies and paid their premiums, only to face unexpected challenges when fires actually struck. This article explains exactly what your policy covers, what it doesn't, and the steps you need to take now to ensure adequate protection.

Having coverage and being fully protected are two different things. The gap between these can have devastating financial consequences.

Does Home Insurance Cover Wildfire? What's Actually Included

Most standard homeowners policies treat wildfire damage the same as any other fire-related loss. Your basic policy provides protection across several critical areas.

Dwelling and Structure Protection

Your home's structure receives coverage under the dwelling portion of your policy. If a wildfire damages or destroys your house, this coverage pays to repair or rebuild it. This represents the foundation of your insurance protection and addresses the primary question homeowners ask: does home insurance cover wildfire destruction to the main structure? In most cases, yes.

Detached structures also receive protection. Your garage, shed, fence, or gazebo falls under "other structures" coverage. Any building on your property that isn't attached to your main residence qualifies for this protection.

Personal property coverage extends to your belongings. Furniture, electronics, clothing, and appliances all receive coverage under this portion of your policy. If fire destroys these items, your insurance helps replace them.

Additional Living Expenses

Many homeowners overlook this coverage until they need it. If your home becomes uninhabitable after a wildfire, your policy covers the cost of temporary housing and related expenses.

This includes hotel stays, rental housing, restaurant meals, and other costs you wouldn't normally incur. This coverage proves invaluable when you're displaced for weeks or months during reconstruction.

The duration and limits vary by policy. Most policies cover these expenses for 12 to 24 months, up to a specified percentage of your dwelling coverage. Review your specific limits now rather than when you're searching for emergency housing.

Replacement Cost Considerations

Standard dwelling coverage may prove insufficient after a major wildfire. When hundreds or thousands of homes require rebuilding simultaneously, construction costs increase dramatically. Understanding whether your policy fully covers rebuilding costs requires examining your specific coverage limits.

Extended replacement cost coverage increases your dwelling limit by an additional 25% to 50%. This buffer helps when material and labor costs spike following a disaster.

Guaranteed replacement cost coverage provides even broader protection. It covers the full cost to rebuild regardless of your dwelling limit. While this represents the gold standard of coverage, it carries higher premiums.

Coverage Limitations and Exclusions

Every homeowners policy contains limitations that can create significant financial gaps.

What's Not Covered

Landscaping receives strict limits under most policies. Standard coverage typically extends to approximately 5% of your dwelling coverage, with individual plant limits of $500 to $1,500 per tree or shrub. If you've invested substantially in your landscaping, this may not fully cover replacement costs. When homeowners ask if insurance covers wildfire damage to landscaping, the answer includes significant restrictions.

Vehicles require separate coverage. Homeowners insurance does not cover vehicles damaged in a wildfire. You need comprehensive auto insurance to file a claim for vehicle fire damage. This requires a separate policy, often with a different insurance carrier.

Intentional damage receives no coverage. If you deliberately start a fire, your policy provides no protection. While this seems obvious, it's an important exclusion to understand clearly.

High-Risk Area Challenges

Homeowners in wildfire-prone zones face increasingly difficult insurance situations. Seven of California's 12 largest home insurers have paused or severely restricted new policies in high-risk areas. Many existing policyholders face non-renewal at their policy expiration date.

Premium increases have become substantial. Rate hikes of 20% to 50% are common, and some areas see even larger increases. Additionally, percentage-based deductibles are replacing flat-dollar amounts. Instead of a $2,000 deductible, you might face 2% to 5% of your home's insured value. On a $500,000 home, that translates to $10,000 to $25,000 in out-of-pocket expenses.

Major insurance carriers are withdrawing from high-risk markets entirely. California, Texas, and Colorado have seen companies like State Farm and Allstate stop writing new policies in fire-prone regions.

Alternative Coverage Options

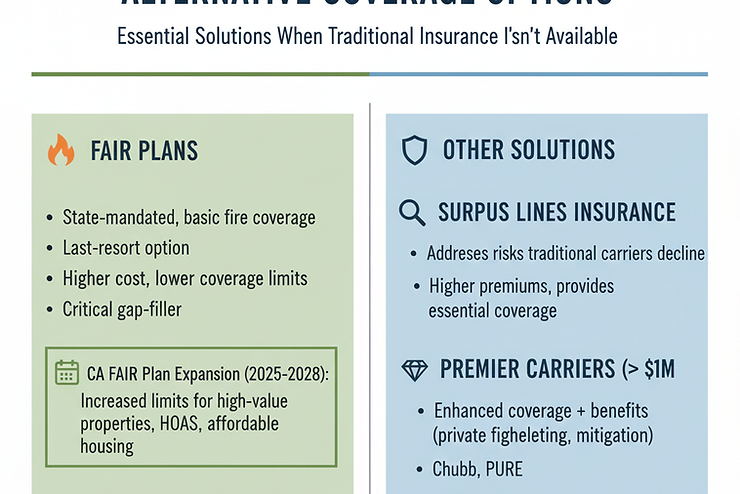

When traditional insurers decline to provide coverage, several alternatives exist. These options typically cost more and provide less comprehensive coverage, but they serve an essential purpose when conventional insurance is unavailable. The question of whether home insurance covers wildfire risk in high-danger zones often leads homeowners to these alternative solutions.

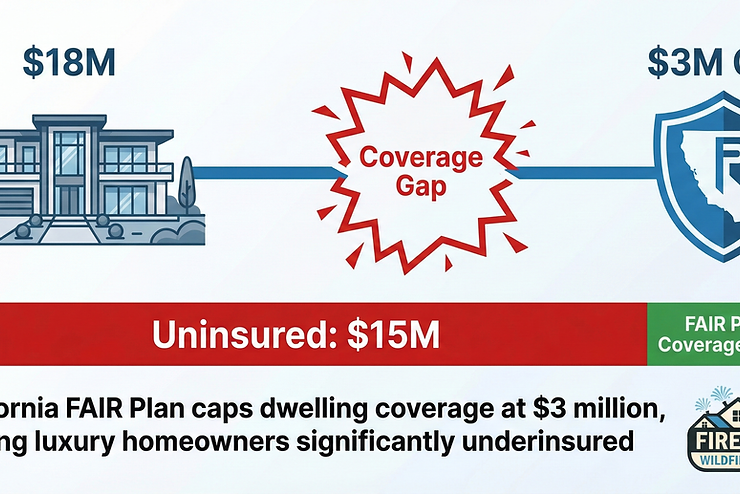

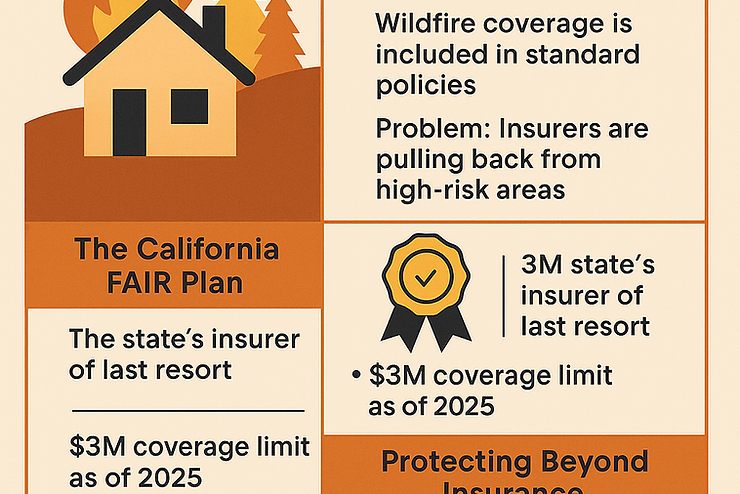

FAIR Plans

FAIR stands for Fair Access to Insurance Requirements. These state-mandated programs provide basic fire coverage when private insurers refuse to issue policies.

By design, FAIR Plans serve as last-resort coverage. They typically cost more than standard policies and offer lower coverage limits. However, when no private insurer will provide coverage, these programs fill a critical gap.

The California FAIR Plan underwent major expansion in 2025. Coverage limits increased for high-value commercial properties, homeowner associations, and affordable housing. These changes remain in effect through 2028 as the state works to stabilize the insurance market.

Other Solutions

Surplus lines insurance addresses risks that traditional carriers won't accept. These policies carry higher premiums but can provide coverage where standard insurers refuse.

Premier carriers specialize in high-value properties. Companies like Chubb and PURE offer enhanced coverage with additional benefits including private firefighting services and wildfire mitigation programs. If your home exceeds $1 million in value, these specialized carriers may be your best option.

How Fire-Resistant Roofing Affects Coverage

Your roof serves as your first line of defense against wildfire. It also represents your most significant opportunity to improve your insurance situation.

Insurance Benefits

Class A fire-rated roofing materials qualify for premium discounts. These materials meet the highest fire resistance standards. Insurers reward their installation because fire-resistant roofing significantly reduces their exposure to claims.

California's Safer from Wildfires regulation requires insurers to offer discounts for home hardening measures. Fire-resistant roofing tops that list. Discounts typically range from 8% to 15% for major insurers, with some carriers offering up to 18% depending on combined mitigation efforts.

Some insurers now require fire-resistant roofing in high-risk zones. It has transitioned from a nice-to-have feature to a baseline requirement for coverage eligibility. Homeowners wondering whether insurance covers wildfire losses need to understand that appropriate roof materials can determine whether they receive coverage at all.

Mitigation Measures That Lower Costs

Defensible space requirements directly impact your insurability. California mandates 100 feet of cleared space around homes in wildfire zones. Maintaining this clearance affects both your ability to obtain coverage and your premium rates.

Non-combustible materials for vents, eaves, and decking reduce ember intrusion. Embers cause the majority of home ignitions during wildfires, rather than direct flame contact. Addressing these vulnerable points provides substantial protection.

Fire detection and suppression systems add another protective layer. Sprinkler systems, foam suppression, and early warning sensors can make the difference between a home that survives and one that burns.

Insurance companies now use satellite imagery and advanced analytics to assess wildfire risk before issuing policies. They can evaluate your roof condition, defensible space, and surrounding vegetation remotely. Poor mitigation measures are immediately visible in these assessments.

Filing a Wildfire Claim

Understanding the claims process before disaster strikes saves time and reduces stress.

Required Steps

Contact your insurer immediately after a wildfire affects your property. Most policies require prompt notification. Call your agent or insurance carrier as soon as safety permits.

Documentation proves essential to claim success. Take photos and videos of all damage before beginning any cleanup. If you can safely access your property, document every room, structure, and damaged item thoroughly.

Proof of loss requirements can be extensive. You'll need to itemize damaged or destroyed property with estimated values and purchase dates. Maintaining a home inventory before a disaster makes this process significantly easier.

2025 Updates

California passed new consumer protections following the Los Angeles fires. Insurers must now provide 60% of contents coverage limits upfront for total losses, capped at $350,000, without requiring a detailed inventory list. This change helps displaced homeowners access funds more quickly.

Extended filing deadlines give survivors additional time to complete their claims. You now have at least 100 days to provide proof of loss after a declared state of emergency.

Smoke damage claim regulations became stricter in 2025. California's Insurance Commissioner issued cease and desist orders against FAIR Plan for denying legitimate smoke damage claims. Insurers must now properly investigate and pay these claims under updated guidelines.

Taking Control of Your Wildfire Protection

Home insurance typically covers wildfire damage, but coverage alone doesn't guarantee protection. The insurance landscape continues to shift rapidly, particularly in California. Carriers are withdrawing from high-risk areas, premiums are increasing substantially, and coverage gaps are widening. You need adequate dwelling limits, extended replacement cost coverage, and a clear understanding of your policy exclusions.

The most effective insurance policy is one you never need to use. Fire-resistant roofing, defensible space, and home hardening measures don't just reduce your premiums. They protect your actual property.

FireRoofs specializes in comprehensive wildfire defense systems that combine fire-resistant roofing with advanced protection technology. Our automated wildfire detection uses cameras with intelligent fire detection to detect wildfire threats around your property. The system analyzes environmental data continuously and sends alerts to your phone when threats are detected. You know what's happening even if you're not home. Along with satellite wildfire alerts and system activation up to 5 miles around your home.

This early warning gives you time to evacuate safely, while your defense systems automatically activate before fire reaches your property. Our automated sprinklers and foam suppression technology create active protection when wildfires threaten.

Investing in real wildfire protection now prevents the need to fight with insurance adjusters later. Review your policy limits today. Upgrade to fire-resistant roofing. Build and maintain your defensible space. Take control before the next fire season arrives.

The question isn't whether home insurance covers wildfire damage. The question is whether you'll have a home left to insure when fires reach your area.

Frequently Asked Questions

Will my homeowners insurance cover smoke damage from a nearby wildfire?

Yes, smoke damage typically receives coverage under standard homeowners insurance policies. California regulations updated in 2025 require insurers to properly investigate and pay legitimate smoke damage claims. Document the damage with photos and file your claim promptly.

What is the average deductible for wildfire damage claims?

Wildfire deductibles vary by location and insurer. Traditional flat-dollar deductibles range from $1,000 to $5,000. High-risk areas increasingly face percentage-based deductibles of 2% to 5% of your home's insured value. That translates to $10,000 to $25,000 out of pocket on a $500,000 home.

Can my insurance company drop me after a wildfire claim?

Insurance companies generally cannot cancel your policy immediately after you file a wildfire claim. However, they can choose not to renew when your policy expires. California implemented a temporary moratorium after the 2025 Los Angeles fires preventing non-renewals in affected areas.

How much does FAIR Plan insurance cost compared to standard homeowners insurance?

FAIR Plan policies typically cost 20% to 50% more than standard homeowners insurance while offering lower coverage limits. The California FAIR Plan proposed average rate increases of 35.8% for 2026. Exact costs depend on your location, home value, and coverage limits.

What home improvements provide the biggest insurance discounts in wildfire zones?

Class A fire-rated roofing provides the largest discounts in wildfire-prone areas, typically 8% to 15% off premiums. Other high-impact improvements include ember-resistant vents, tempered windows, non-combustible decking, and maintaining 100 feet of defensible space. Advanced systems with automated detection and automated sprinklers can provide additional discounts.

Don't wait until the next fire season to secure your property. FireRoofs provides complete wildfire defense solutions tailored to California's high-risk environments. Our systems integrate smooth with your existing home while providing 24/7 automated protection.

Ready to learn more about protecting your home and potentially lowering your insurance premiums? Visit our FAQ page for detailed answers about our systems, installation process, and pricing.

Want to discuss your specific property needs? Contact our team for a free consultation. We'll assess your wildfire risk and design a defense system that fits your home and budget.

FireRoofs.com - Advanced Wildfire Defense Systems for California Homes