Your Policy Covers $3M. Your Rebuild Costs $8M.

Carriers are leaving California. The FAIR Plan caps at $3 million. Bay Area homes cost $5 million to $10 million to rebuild. That gap is not a technicality. It is the difference between recovery and financial ruin.

We cannot fix your insurance. But we can make sure your house is still standing when the fire passes. That changes the math entirely.

The Rebuild Gap

For a typical Bay Area WUI luxury home

700K+

Policies lost since 2019

85%

Homes lost in first 90 min

$450B

FAIR Plan exposure

Wildfire Insurance in California: What Homeowners Actually Need to Know

California's Wildfire Insurance Crisis

700,000+

California homeowners have lost private wildfire insurance coverage since 2019

5,600

Homes destroyed by wildfire per year on average in California

$3M

Maximum dwelling coverage under the FAIR Plan

7 of 10

Most destructive California wildfires in history occurred in the last decade

Multiple

Major carriers have pulled out of or restricted WUI policies across California

85%

Of Palisades Fire structures lost in the first 90 minutes, before fire crews could reach most homes

What the FAIR Plan Actually Covers

The FAIR Plan caps residential coverage at $3 million. In the Bay Area WUI, that gap between policy limit and actual property value is where homeowners get destroyed financially. A home appraised at $8 million, $12 million, or $15 million is insured for a fraction of what it would cost to rebuild. That is not a technicality. It is the difference between recovery and financial ruin.

The FAIR Plan covers basic fire and smoke damage to the structure. That is it. It does not cover liability, personal property, loss of use, or additional living expenses while you rebuild. If you are forced to rent housing for 18 months during reconstruction, that cost comes entirely out of pocket. If a visitor is injured on your property during a fire event, you have no liability coverage.

The rebuild cost gap is the number most homeowners underestimate. Construction costs in the Bay Area run $400 to $600 per square foot for luxury homes. A 5,000 square foot estate costs $2 million to $3 million to rebuild at current rates, before site prep, landscaping, and extended timelines. A $3 million FAIR Plan payout does not cover that. Homeowners who rely on the FAIR Plan as their only coverage are accepting a gap they may never close.

How Documented Mitigation Changes the Insurance Conversation

This is the part most homeowners miss. California law does not just protect you from non-renewals. It actively requires insurers to recognize mitigation. Under Insurance Code Section 2644.9 (Safer from Wildfires), admitted carriers must offer premium discounts for documented wildfire mitigation across 12 specific categories.

The problem is documentation. Most homeowners have done some hardening work but have no organized evidence to show an underwriter. That is where FireRoofs comes in. We build the systems, complete the hardening, and deliver the documentation. Your insurer or broker handles the rest.

We do not act as insurance brokers or agents. We do not provide insurance advice or place policies. We build the systems, complete the hardening, and deliver the documentation package that gives your broker the strongest possible case.

Three Flexible Pathways Based on Your Insurance Situation

Insurance Deadline Response

Facing non-renewal with a tight deadline? We prioritize emergency defensible space clearing (Zone Zero plus 100 feet), ember-resistant vent installation, and basic documentation for your non-renewal appeal. This is the fastest pathway to demonstrate immediate mitigation when your carrier gave you 30 to 90 days.

FAIR Plan Exit Strategy

Stuck on the FAIR Plan paying double premiums? We target the specific mitigation categories that give your broker the strongest case when shopping your property to standard carriers: defensible space, Zone Zero clearing, ember-resistant vents, noncombustible fencing, and roof assessment. Sprinklers can be added in this phase or later.

Integrated Protection

Full budget flexibility? We install automated exterior sprinklers, complete all home hardening work, and deliver the premier documentation package. This is the comprehensive approach where everything is done together under one coordinated timeline.

Documentation at every phase. We document every phase of work as it is completed. You do not wait until everything is done to start submitting documentation. Partial mitigation, properly documented, earns immediate discounts.

Common Insurance Questions

Does installing a wildfire defense system lower my insurance premium?

California's Safer from Wildfires framework requires participating insurers to offer discounts for homes that meet specific mitigation standards. A documented exterior sprinkler system qualifies under multiple categories. The discount amount varies by carrier. The evidence packet we provide after installation is formatted specifically for underwriting review and is designed to support that conversation with your broker.

Will the FAIR Plan recognize my system?

The FAIR Plan does not currently offer premium discounts for wildfire mitigation systems the way admitted carriers do. However, a documented and installed system strengthens your reinstatement case with private surplus lines carriers, which is the goal for most WUI homeowners. The objective is getting off the FAIR Plan, not managing it.

What documentation do I need to show my carrier?

Carriers evaluating risk mitigation need: system engineering specifications, component manufacturer certifications, activation testing records, detection coverage maps, and annual maintenance logs. After installation, we compile all of this into a single evidence packet formatted for underwriting review. You provide it to your broker and they present it to the carrier.

You Live in the WUI. Here's What That Means.

WUI stands for wildland-urban interface. It's where developed neighborhoods meet undeveloped wildland. Grass, brush, timber. If your backyard touches open hillside or your driveway runs through trees, you're in it.

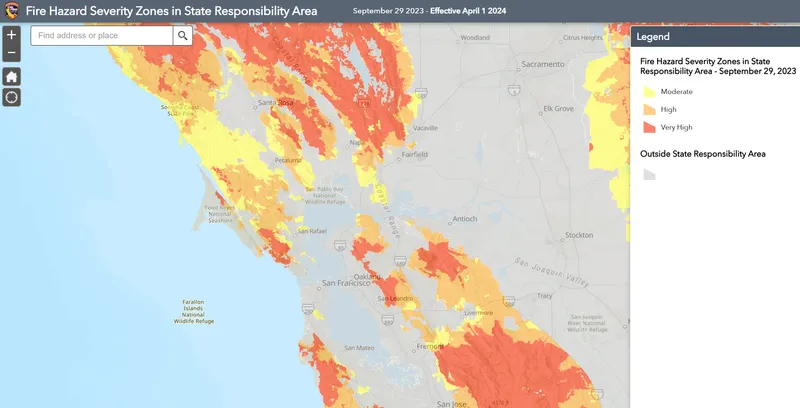

California's Fire Hazard Severity Zone maps (maintained by CAL FIRE) classify properties as Moderate, High, or Very High risk. Most of the communities FireRoofs serves, Saratoga, Los Gatos, Woodside, Portola Valley, the Santa Cruz Mountains, fall in the Very High Fire Hazard Severity Zone (VHFHSZ).

That classification directly affects your insurance. Carriers use FHSZ data in underwriting decisions. A VHFHSZ designation is one of the primary triggers for non-renewal notices and policy restrictions. It's not personal. It's actuarial. But the result is the same: you're left holding more risk than you think.

Bay Area Fire Hazard Severity Zones (CAL FIRE)

The FAIR Plan Was Never Meant to Be Your Insurance

The California FAIR Plan (Fair Access to Insurance Requirements) is a state-mandated pool that provides basic fire coverage to homeowners who can't find it on the private market. It was designed as a temporary safety net, not a permanent replacement for comprehensive homeowner's insurance. Here's where it falls short for luxury homeowners:

Dwelling coverage caps at $3 million.

If your rebuild cost exceeds that, and in most Bay Area WUI communities it does, the gap is your problem.

No liability coverage.

FAIR Plan policies are fire-only. You still need a separate policy (called a DIC, Difference in Conditions) for liability, theft, water damage, and everything else a standard homeowner’s policy covers. That’s a second premium on top of an already expensive one.

Limited personal property coverage.

Contents coverage maxes out well below what most luxury homeowners actually own.

Premiums are rising fast.

FAIR Plan rates have increased significantly year over year. The plan’s total exposure has grown from roughly $150 billion to over $450 billion since 2020. That growth isn’t sustainable without rate increases, and they’re coming.

FAIR Plan enrollment surged past 600,000 policies by mid-2025. Over 788,000 homeowner policies were non-renewed in 2023 alone. For homes in Very High Fire Hazard Severity Zones, which includes the majority of communities like Saratoga, Woodside, and Los Gatos, private coverage is increasingly available only through surplus lines carriers who charge higher premiums and require documented risk mitigation as a condition of writing the policy.

The bottom line: The FAIR Plan keeps a roof over your head on paper. It doesn't come close to making you whole after a loss.

The Carriers Aren't Coming Back

This isn't a temporary market correction. This is a structural shift.

2019-2020

After the Camp Fire and multiple billion-dollar wildfire seasons, major carriers begin restricting new policies in WUI zones across California.

2021-2022

Non-renewal waves hit tens of thousands of policyholders. Major carriers reduce WUI exposure across the state. The FAIR Plan enrollment surges.

2023

The largest homeowner’s insurer in California announces it will no longer accept new applications in the state. Walking away from new business entirely.

2024

High-net-worth carriers tighten underwriting in VHFHSZ areas. Military family insurers restrict coverage in fire zones. The FAIR Plan’s total insured exposure crosses $400 billion.

2025-2026

The Palisades Fire causes an estimated $30-50 billion in insured losses. California Insurance Commissioner pushes reforms, but the market hasn’t stabilized. Private carriers remain cautious. The FAIR Plan remains the default, and the gap keeps growing.

Insurance Won't Save Your House. Defense Might.

Here's what no insurance company will tell you: the best way to protect your financial position in a wildfire isn't a better policy. It's making sure your house is still standing after the fire passes.

That changes the math entirely.

A home that survives a wildfire doesn't file a total-loss claim. It files a much smaller claim, or no claim at all. That's good for you, good for your carrier, and good for your renewal odds.

Some carriers and surplus-lines underwriters are beginning to factor active wildfire defense systems into their risk assessments. We're not going to overstate this. There's no industry-wide “FireRoofs discount” yet. But we are seeing:

- Underwriters asking whether homes have exterior sprinkler systems

- Surplus-lines carriers offering coverage in zones where admitted carriers won’t, partly based on physical mitigation measures

- Insurance brokers recommending defense systems as part of a package to demonstrate reduced risk to carriers

- Homeowners using defense system documentation to appeal non-renewal decisions

The trend line is clear: the insurance industry is shifting toward rewarding physical mitigation, not just defensible space. FireRoofs puts you ahead of that curve.

See how the system works90

Minutes. Maybe Less.

The Palisades Fire proved what fire scientists have warned about for years: when a wildfire hits an urban area, the destruction happens fast. Most structures are lost in the first 60 to 90 minutes, before fire crews can reach them.

That's the window where your home is on its own.

FireRoofs systems are designed for exactly this scenario. When embers arrive and flames approach, the system is already running. Sprinklers are saturating the roof and walls. Foam is coating the eaves. The vegetation perimeter is soaked. Your house is buying time that fire crews don't have to give you.

We can't guarantee your home survives every fire. Nobody can. But we can make sure it's fighting back during the minutes that matter most.

What Makes This System Insurance-Grade

Every component is documented, tested, and formatted for carrier review.

Dual-Detection Monitoring

Satellite regional monitoring plus on-property intelligent cameras. Two independent detection layers exceed standard single-sensor requirements.

Automated Three-Level Response

Pre-wetting, intensive saturation, and maximum defense with optional Class A foam injection. Foam is 100% biodegradable, non-toxic to plants, pets, and wildlife, and rinses off through the sprinklers. Each level triggers automatically based on verified threat data. No manual intervention required.

Redundant Water Supply

Auto-switching water source fail-safe. If municipal pressure drops below threshold, system automatically switches to pool or storage tank pump. Continuous operation guaranteed.

Satellite Communication Backbone

Starlink satellite communication keeps the system connected and reporting when local internet and cell service go down during wildfire events. For properties without backup power, we recommend adding a generator or home battery to maintain sprinkler operation during extended outages.

California Law Requires Insurers to Recognize Mitigation

Under Insurance Code Section 2644.9 (Safer from Wildfires), admitted carriers must offer premium discounts for documented wildfire mitigation. The FAIR Plan also offers up to 12 individual discounts on the wildfire portion of premiums.

Admitted Carriers

Required by Section 2644.9 to discount for 12 CDI mitigation categories

California FAIR Plan

Up to 16.4% off wildfire premium portion for qualifying policyholders

E&S / Surplus Lines

Evidence packets support underwriting review and voluntary market placement

Your Carrier-Ready Evidence Packet

Every FireRoofs installation includes a comprehensive evidence packet at commissioning. Designed for insurers, underwriters, and risk engineers to evaluate without a site visit.

AB 888: The California Safe Homes Act (2026)

AB 888 establishes a grant program through the California Department of Insurance to help qualifying homeowners fund fire-safe roofs and Zone Zero mitigation, the 0-5ft ember-resistant zone immediately around the home. The program prioritizes roof replacement and Zone Zero work, both of which align directly with what FireRoofs protects.

Passive Zone Zero clearing removes fuel. That is necessary but not sufficient. FireRoofs adds active automated saturation of that same zone, providing a layer of defense that clearing alone cannot deliver. When embers land in a cleared Zone Zero, the ground is dry. When embers land in a FireRoofs-protected Zone Zero, the ground, walls, eaves, and roof are already wet. That difference determines whether your home ignites or survives.

SB 429 - California's New Public Wildfire Risk Model

In October 2025, Governor Newsom signed SB 429 into law, establishing the nation's first public wildfire catastrophe model. Effective January 1, 2026, the California Department of Insurance is charged with funding a university-led consortium to build a transparent, publicly accessible model that simulates wildfire property damage and generates risk scores homeowners can actually see and act on.

This matters for San Francisco Bay Area WUI homeowners because insurance carriers have long used private, proprietary models to justify rate increases and non-renewals without explaining the underlying risk calculations. SB 429 creates a public benchmark so homeowners, regulators, and legislators can evaluate whether those rate decisions are accurate.

The model itself is still in development. The CDI released its grant process framework in late 2025 and expects to issue a full Request for Proposals to university consortiums in Q2 2026. Track current milestones at insurance.ca.gov.

Homeowners who have documented exterior fire mitigation measures on their property will be best positioned to benefit from the transparency this model creates. Ask HydroIQ about SB 429 and what it means for your specific county and fire zone.

The $7M+ Gap Nobody Talks About

The FAIR Plan caps residential coverage at approximately $3M (effectively $3-3.3M with available endorsements). A $10M Bay Area estate insured under the FAIR Plan has a $7M+ gap. No policy covers that. No rider fills it. No umbrella extends to it.

The only way to close the gap is to prevent the loss in the first place. That is the function of a FireRoofs exterior fire sprinkler system. It does not replace insurance. It makes insurance viable again by reducing the risk that your carrier is underwriting.

How the System Works

Three-stage automated defense with dual wildfire detection.

Common Questions

42 answers about detection, installation, cost, and insurance benefits.

Proven Results

Real installations protecting Bay Area estates.

Evidence Packet Details

Documentation formatted for carrier underwriting review.

Related Resources

Your Coverage Has a Gap. Let's Close It.

The right documentation changes the conversation with your carrier. Book a free evaluation and we'll show you what an insurance-grade defense system looks like for your property.

Not ready to talk yet? Check your property's wildfire risk score first.

Free Wildfire Assessment ReportNot sure about your insurance options? Ask HydroIQ

HydroIQ can explain FAIR Plan coverage limits, Difference in Conditions policies, what documentation carriers want to see, and how an exterior sprinkler system may help you regain private coverage. Free, instant, no sign-up required.

Stay Ahead of Fire Season

Insurance updates, carrier news, WUI policy changes, and wildfire preparedness. Delivered monthly. No spam. No fluff.

Common Questions

Does wildfire defense lower my homeowners insurance premium?

Many homeowners in wildfire-prone areas struggle to find or keep coverage. While premium impacts vary by carrier and policy, having a professionally installed wildfire defense system demonstrates proactive risk mitigation. The FAIR Plan caps coverage at $3 million, which often falls far short of actual rebuild costs for homes valued at $5 million and above.

Are roof sprinklers required by California fire codes in WUI zones?

Exterior wildfire sprinkler systems like FireRoofs are voluntary upgrades, not code-mandated. California building codes require interior fire sprinklers in new residential construction, but exterior wildfire defense is a separate category that homeowners choose to add for protection beyond code minimums.

What are AB 888 and SB 429, and how do they affect homeowners?

AB 888, the California Safe Homes Act, provides grant funding for Zone Zero hardening and fire-safe roofing improvements. SB 429 establishes the Wildfire Public Catastrophe Model to bring transparency to how wildfire risk is assessed in insurance. Both took effect January 1, 2026.

Find Out Where Your Property Stands

Wondering how your home measures up against California wildfire codes? Our satellite pre-assessment gives you a quick look at your roof, vegetation, and fire zone. If you want a full assessment with code citations, that is available too.

- Satellite imagery of your property and defensible space

- Fire zone and WUI classification lookup

- Documentation you can share with your broker

Takes about a minute. No account needed.